🔴 BREAKING: Prime Minister Shehbaz Sharif officially launched the PM Apna Ghar Programme on 30 April 2026 in Islamabad, distributing the first cheques to successful applicants of Phase 1. This is the largest federal housing finance scheme in Pakistan's history, Rs 3.2 trillion in total financing for 500,000 homes nationwide.

For most Pakistanis, owning a home has felt like a dream that quietly slipped further away every year. Rents kept climbing, construction costs nearly doubled in two years, and bank loans demanded markups of 22% or more. The new federal Wazir-e-Azam Apna Ghar Programme, Ghar Ho Tu Apna is the government's most serious answer to that crisis to date. With a fixed 5% markup for ten years, loans up to Rs 10 million, and 20-year repayment, this is the first time a federal scheme has been priced for working-class families instead of property investors.

This guide covers everything you need to know, loan slabs, exact monthly installments, eligibility, the four banks already onboard, the application process, and the differences between this federal programme and the Punjab-only Apni Chhat Apna Ghar scheme.

Quick Facts: PM Apna Ghar Programme at a Glance

| Detail | Information |

|---|---|

| Official Name | Wazir-e-Azam Apna Ghar Programme, Ghar Ho Tu Apna |

| Launched By | Prime Minister Shehbaz Sharif |

| Launch Date | 30 April 2026 (Islamabad) |

| Total Allocation | Rs 3.2 Trillion |

| Target Units | 500,000 housing units (50,000 in Year 1) |

| Loan Slabs | Rs 2.5M / 5M / 7.5M / 10M |

| Markup Rate | 5% fixed for first 10 years, KIBOR + 3% thereafter |

| Repayment Period | Up to 20 years |

| Financing Split | 90% bank-financed, 10% applicant equity |

| Property Limit | House up to 10 marla / Flat up to 1,500 sq. ft. |

| Coverage | All 4 Provinces + Islamabad + Gilgit-Baltistan + Azad Kashmir |

| Official Portal | apnaghar.gov.pk |

| Approval Timeline | 15 working days (bank-side) |

| Application Fee | Zero, no fee, no upfront cost |

| Monitoring | State Bank of Pakistan + Pakistan Housing Authority Foundation |

What Is the PM Apna Ghar Programme?

The PM Apna Ghar Programme is a markup subsidy and risk-sharing scheme notified by the State Bank of Pakistan under SH&SFD Circular No. 03 of 2025. It provides subsidised, long-term housing finance to first-time homeowners across Pakistan. Unlike previous schemes such as Mera Pakistan Mera Ghar (which was suspended after running out of funds), this programme is structured as a permanent federal initiative with annual budget allocations.

The scheme is delivered through participating commercial banks, Islamic banks, microfinance banks, and the House Building Finance Company (HBFC), but the risk is shared with the federal government, which is what allows banks to offer the 5% rate. Without the government taking on part of the credit risk, no bank in Pakistan would offer a 20-year mortgage at 5% in the current economic environment.

The government's slogan for the programme, "Ghar ho tu apna", captures the social goal: every working family deserves a home of its own, not someone else's.

Loan Slabs and Monthly Installments (Verified)

These are the exact loan slabs and monthly installments confirmed by the Prime Minister's Office on 30 April 2026:

| Loan Amount | Property Type Covered | Monthly Installment | Tenure |

|---|---|---|---|

| Rs 2,500,000 | Smaller home / 3-marla construction | Rs 16,499 | Up to 20 years |

| Rs 5,000,000 | 5-marla home or 1,000 sq ft flat | Rs 32,997 | Up to 20 years |

| Rs 7,500,000 | 7-marla home or larger flat | Rs 49,497 | Up to 20 years |

| Rs 10,000,000 | Up to 10-marla home / 1,500 sq ft flat | Rs 65,996 | Up to 20 years |

Important: These installment figures are based on the fixed 5% markup applicable for the first 10 years. After year 10, the rate transitions to 1-year KIBOR + 3%, which means your monthly installment may change based on prevailing market rates at that point. Banks must clearly disclose this re-pricing schedule before you sign.

What Does the Loan Cover?

Under the programme, the financing can be used for any one of the following four purposes:

- Purchase of a constructed house (up to 10 marla)

- Purchase of a flat (up to 1,500 sq. ft.)

- Purchase of a residential plot (up to 10 marla) along with construction

- Construction on a plot you already own (up to 10 marla)

Plot-only purchase without construction is not allowed. Pure renovation finance is also not covered under the federal programme, you would need to look at conventional bank products for that.

Eligibility Criteria for PM Apna Ghar Programme

The eligibility rules are deliberately wider than the Punjab ACAG scheme because the federal programme targets a broader middle-income segment, not only the poorest households.

Mandatory Requirements:

- Applicant must be a resident Pakistani citizen holding a valid CNIC

- Must be a first-time homeowner (no residential property currently in your name anywhere in Pakistan)

- Age between 25 and 60 years at the time of loan maturity for salaried individuals; 25 to 65 years for self-employed individuals

- Clean credit history, no record of loan default with any bank or DFI

- Stable, verifiable income, salary slip, business income, or remittance proof

- Must be able to provide the 10% equity contribution (e.g., Rs 250,000 on a Rs 2.5M loan, Rs 1,000,000 on a Rs 10M loan)

- The financed property must be legally clear with verified ownership documents

Special Categories Welcome:

- Salaried individuals (SI), government and private sector employees

- Self-employed professionals (SEP), doctors, lawyers, engineers, consultants

- Self-employed businessmen (SEB), shop owners, traders, small business owners

- Non-Resident Pakistanis (NRPs), apply via the Roshan Apna Ghar track requiring a Roshan Digital Account

Important Note: Owning agricultural land or a commercial shop does NOT disqualify you. The "first-time homeowner" rule applies only to residential property in your name.

Required Documents

Gather these before starting your application, incomplete files are the #1 reason applications get delayed.

Identity Documents:

- Original CNIC (and spouse's CNIC if married)

- Recent passport-sized photographs (2-4 copies, blue/white background)

Income & Financial Proof:

- Last 6 months' salary slips (for salaried)

- Last 12 months' bank statements

- Tax returns (for self-employed)

- NTN certificate (where applicable)

- Employer letter (for salaried)

Property Documents:

- Sale agreement / proposed property title document

- Fard / Registry / Allotment letter

- Approved building plan (for construction)

- NOC from the housing society or development authority (where applicable)

Equity & Down Payment Proof:

- Bank statement showing the 10% equity amount available

- Source-of-funds declaration

Legal Compliance:

- Affidavit declaring no other residential property

- Reference letters (one personal, one professional)

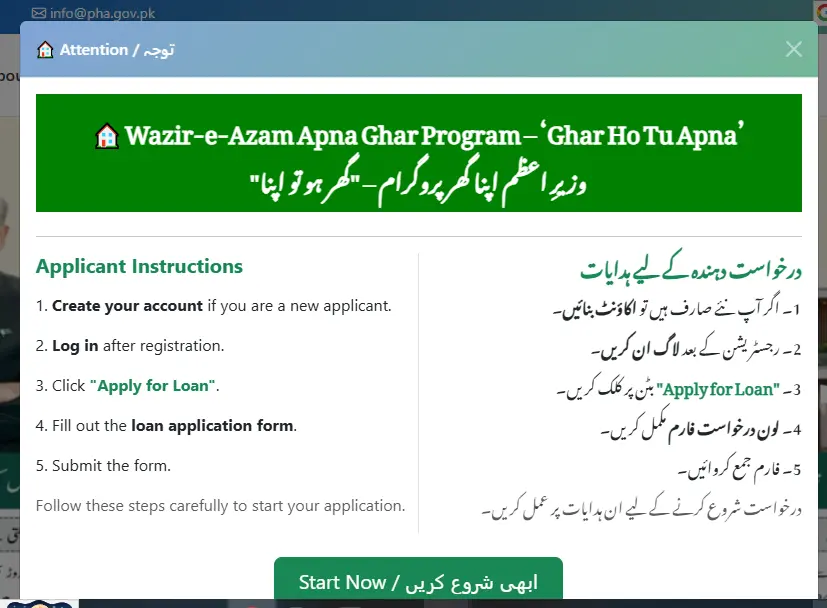

How to Apply for PM Apna Ghar Programme, Step-by-Step

Step 1: Visit the Official Portal

The only official application portal is apnaghar.gov.pk. Be cautious, several lookalike domains have already appeared since the launch. The official portal is hosted on the .gov.pk domain and links from the State Bank of Pakistan's official website.

Step 2: Create Your Account

Click "Register" on the homepage. You will be asked for:

- 13-digit CNIC (no dashes)

- Mobile number registered in your name

- Active email address

- A strong password

You will receive an OTP via SMS for mobile verification, and a confirmation link via email. Both must be verified before you can proceed.

Step 3: Complete the Application Form

Once logged in, the application form is divided into four sections:

- Personal Details, name, date of birth, marital status, dependents

- Income & Employment, employer/business details, monthly income, other income sources

- Property Requirements, type of financing (purchase/construction), preferred location, estimated property value

- Loan Selection, choose your loan slab (Rs 2.5M / 5M / 7.5M / 10M) and preferred bank

Step 4: Upload Required Documents

Upload all documents listed above as clear PDF or JPG files (each under 2 MB). Blurry or partial scans will be rejected at verification.

Step 5: Choose Your Bank

You'll see a list of participating banks. As of May 2026, confirmed participants include:

- Allied Bank Limited (ABL), all branches designated

- Bank Alfalah, Islamic and conventional both

- Bank of Punjab (BOP)

- House Building Finance Company (HBFC)

- Meezan Bank (Islamic financing)

- Bank AL Habib

The Prime Minister has stated banks will be ranked publicly on disbursement speed, with national awards given on 14 August 2026 to top-performing banks.

Step 6: Submit and Track

After submission, you receive a Tracking ID, save this. The bank you selected will contact you within 3,5 working days for property valuation and document verification.

Step 7: Approval and Disbursement

Banks have been mandated to complete approvals within 15 working days of receiving a complete application. For loans up to Rs 5 million, the bank can use its in-house valuation. For loans above Rs 5 million, an approved third-party valuer is mandatory.

After approval:

- For purchase: funds disbursed directly to seller

- For construction: funds released in construction-linked tranches as work progresses

Phase 1 Targets and First-Year Plan

The Prime Minister has confirmed concrete first-year targets:

- First-year financing target: 50,000 homes

- First-phase budget allocation: Rs 321 billion

- First batch of cheques: Already distributed at the 30 April launch ceremony in Islamabad

- Geographic priority: All four provinces simultaneously, with quotas to be announced by SBP

- Personal monthly review: PM Shehbaz Sharif has committed to personally reviewing programme progress every month

The government's stated four-year goal is 500,000 homes built, with an estimated economic impact of 2 million construction jobs created and a multiplier effect across cement, steel, ceramics, and electrical industries.

PM Apna Ghar (Federal) vs Apni Chhat Apna Ghar (Punjab), Which One Should You Apply For?

This is the question we get most often, because the names are confusingly similar. Here's the clear comparison:

| Feature | PM Apna Ghar Programme (Federal) | Apni Chhat Apna Ghar (Punjab) |

|---|---|---|

| Launched By | PM Shehbaz Sharif | CM Maryam Nawaz |

| Coverage | All Pakistan + GB + AJK | Punjab only |

| Loan Amount | Rs 2.5M, Rs 10M | Rs 1.5M maximum |

| Markup | 5% fixed (10 years), then KIBOR+3% | 0% interest-free |

| Tenure | Up to 20 years | 7,9 years |

| Income Limit | Verifiable stable income | Less than Rs 60,000/month household |

| Property Limit | Up to 10 marla / 1,500 sq ft | Up to 5 marla urban / 10 marla rural |

| PMT Score Required | Not required | Must be 60 or below |

| Equity | 10% applicant contribution | None for landowners |

| Best For | Middle-income, salaried/professional | Low-income, asset-poor families |

| Portal | apnaghar.gov.pk | acag.punjab.gov.pk |

Quick rule of thumb: If your household income is under Rs 60,000/month and you already own a small plot in Punjab, ACAG is better, it's truly interest-free. If you're a salaried professional anywhere in Pakistan looking to buy a 5,10 marla home, the federal PM Apna Ghar Programme is your route.

You can also apply to both if you qualify, but you can only avail one final loan disbursement.

Important Updates and Latest News

- 30 April 2026: Programme officially launched at PM House in Islamabad. First cheques distributed to Phase 1 beneficiaries.

- Bank performance ranking announced: Banks that lead in disbursement will be honored with national awards on Independence Day (14 August 2026).

- Anti-delay mandate: PM Shehbaz publicly warned banks that "those who step back from their responsibility under the law should not expect favorable treatment" from the federal government.

- No prepayment penalty: You can settle the loan early without any extra charges, a rare feature in Pakistani housing finance.

Common Mistakes to Avoid

After studying competitor sites, news reports, and the SBP circular, here are the avoidable mistakes that cause applications to fail:

- Applying through fake websites. Many copycat domains have appeared, only use apnaghar.gov.pk. The .gov.pk extension is the only authentic indicator.

- Submitting blurry document scans. Banks reject these without notice.

- Hiding existing residential property. The system cross-checks NADRA and excise records, disqualification is permanent if caught.

- Not having the 10% equity ready. Without proof of equity in your bank account, your application stalls at verification.

- Applying through someone else's CNIC. The CNIC must match all property and income documents exactly.

- Choosing a bank by name alone. Different banks process at different speeds, check the disbursement leaderboard before selecting.

Frequently Asked Questions

The programme was officially launched by Prime Minister Shehbaz Sharif on 30 April 2026 at PM House in Islamabad, with the first batch of cheques distributed to Phase 1 beneficiaries during the ceremony. The programme is now actively accepting applications.

The maximum loan is Rs 10 million, available in four slabs: Rs 2.5M, Rs 5M, Rs 7.5M, and Rs 10M. The slab you qualify for depends on your income, equity contribution, and the property value being financed.

The markup is 5% fixed for the first 10 years. After year 10, it transitions to 1-year KIBOR + 3%, which is a market-linked rate. The government provides a markup subsidy during the first 10-year period.

Any resident Pakistani citizen aged 25,60 (or 65 if self-employed) with a valid CNIC, stable income, clean credit history, and no prior residential property in their name. Both salaried and self-employed individuals can apply, including NRPs through the Roshan Apna Ghar track.

Visit apnaghar.gov.pk, register with your CNIC and mobile number, complete the four-section application form, upload required documents, choose a participating bank, and submit. The bank will contact you within 3,5 working days, and approval is mandated within 15 working days.

Confirmed participants include Allied Bank, Bank Alfalah, Bank of Punjab, HBFC, Meezan Bank, and Bank AL Habib. Both Islamic and conventional financing options are available. The full list is updated on apnaghar.gov.pk.

Yes. Non-Resident Pakistanis (NRPs) holding NICOP can apply through the Roshan Apna Ghar track, which requires opening a Roshan Digital Account (RDA) with a participating bank such as Allied Bank or Bank AL Habib. Tenure is extendable up to 25 years for NRPs.

No, the federal scheme is not interest-free, it has a fixed 5% markup for 10 years. The interest-free option is the Punjab Apni Chhat Apna Ghar (ACAG) scheme, which is separate and available only to Punjab residents with a PMT score of 60 or below.

The monthly installment for a Rs 5 million loan at 5% markup over 20 years is Rs 32,997. This is the fixed amount during the first 10 years; the figure may be revised in years 11,20 based on then-prevailing KIBOR rates.

PM Apna Ghar is a federal scheme for all of Pakistan with loans up to Rs 10M at 5% markup. Apni Chhat Apna Ghar is a Punjab-only scheme offering interest-free loans up to Rs 1.5M to low-income families with a PMT score of 60 or below. They are administered by different governments and have different eligibility rules.

No. The Prime Minister has confirmed there are no application fees, processing fees, or upfront costs to apply for the PM Apna Ghar Programme. Be wary of any agent or website charging a registration fee, this is fraud.

Banks have been mandated by the Prime Minister to complete approvals within 15 working days of receiving a complete application. Delays beyond this are subject to government review.

Yes. The scheme has no prepayment penalty, meaning you can settle the outstanding principal early without any extra charges, a major advantage over conventional housing loans.

You can re-apply once you address the rejection reason (typically incomplete documents, equity shortfall, or credit history issue). The bank is required to provide a written reason for rejection. You may also approach a different participating bank for a fresh review.

Watch Out for Scam Websites

Within hours of the 30 April launch, lookalike websites and Facebook pages started appearing claiming to "register" people for a fee. Do not trust them. The real portal has these characteristics:

- ✅ Domain ends in .gov.pk (specifically

apnaghar.gov.pk) - ✅ Linked from State Bank of Pakistan's official website

- ✅ No registration fee, ever

- ✅ No agent calls demanding processing money

If anyone asks for money to "guarantee" your loan approval, walk away, the programme is administered by the State Bank of Pakistan and the Pakistan Housing Authority Foundation, not by private agents.

Final Word: The Window Is Open Right Now

The PM Apna Ghar Programme is the most accessible federal housing scheme Pakistan has launched in over a decade. The combination of 5% fixed markup, 20-year tenure, 90% financing, and zero application fees genuinely lowers the barrier to homeownership for working-class and middle-class families.

The first-year target is 50,000 houses, but early applicants will be processed first. With the Prime Minister personally reviewing progress every month and banks under mandate to clear applications in 15 working days, this is one of the rare government schemes where speed is on the applicant's side.

Start your application today at apnaghar.gov.pk, or visit any branch of Allied Bank, Bank Alfalah, BOP, HBFC, Meezan, or Bank AL Habib.

For more guidance on related schemes and step-by-step help, read our other guides:

- Apna Ghar Online Registration 2026, Form, Last Date & Login

- Apna Ghar Loan Calculator, Rs 2.5M to Rs 10M Monthly Payments

- PM Apna Ghar vs Apni Chhat Apna Ghar, Which One Should You Apply For?

Disclaimer: This article is informational only and does not constitute financial advice. The PM Apna Ghar Programme is administered solely by the State Bank of Pakistan and the Pakistan Housing Authority Foundation. Always apply through official channels at apnaghar.gov.pk or at participating bank branches. Information verified from PM Office press releases (30 April 2026), State Bank of Pakistan SH&SFD Circular No. 03 of 2025, and Allied Bank product documentation.